Ep. 214 – Market Update June 2023 – Interest Rate Increases Yet to Dampen the Market, Sydney Soars, Investor Exodus & Regional Surprises

Ep. 214 – Market Update June 2023 – Interest Rate Increases Yet to Dampen the Market, Sydney Soars, Investor Exodus & Regional Surprises

Mike kicks off our episode with the fresh announcement of our new RBA Governor. The trio wish Michelle the very best in her new role, and they also chat about the departure of Philip Lowe and the key mistake that likely drove the change in Governor.

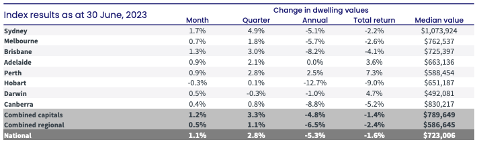

Mike points out that the overall national increase of 1.1% is not really a national story and Cate reinforces that the strength of the Sydney market is driving much of this positive growth data.

Dave also draws regional performance to our listeners’ attention. The capital cities are outperforming the regions; a twist that we have been anticipating but haven’t seen for quite some time. The pace of growth across the board has slowed down, however, and this could be apportioned to the continued rate rises through June.

Internal migration patterns have normalised; our rate of moving to the regions has certainly calmed down since COVID lockdowns. In some cities (such as Melbourne) we are seeing some elasticity and people are returning to the city.

Cate shares an interesting observation from her coalface. She is taking enquiry from quite a few Sydneysiders who are either investing in Melbourne, or moving to Melbourne. The disparity between the two biggest cities is greater how than historical ratios, and Sydneysiders are obviously seeing value in the Melbourne market now that the differential is higher. Cate also mentions that established, boutique units in the Melbourne market seem to be demonstrating capital growth too, and this is something that Melbourne hasn’t experienced for over a decade.

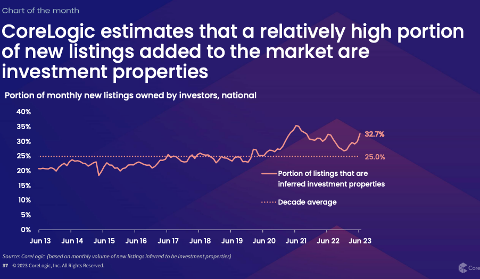

Mike has been chatting to many business owners and property managers about the proportion of sales that are investor-owned properties. Rent rolls are eroding as many investors opt out of property, and anecdotally this is obvious across the board in many cities, but particularly in Victoria.

“The sales department are basically setting fire to their rent rolls…maintaining rent rolls as a steady source of listings,” says Mike.

Source: Core Logic

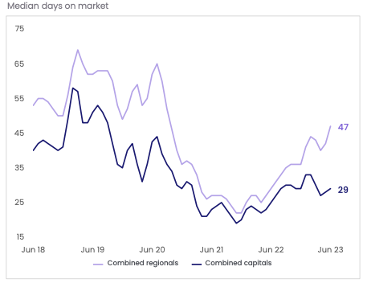

The Trio look at the ‘days on market’ data but Cate uncovers a key reason why this data isn’t neccessariliy a perfect reflection of buyer/seller demand. In auction-centric markets, agents have strong control over the type of campaign that a property can be sold by. Auction campaigns have a usual four week lead time until the sale date, and surely this data skews the data.

“It’s not an organic reflection; it’s deliberately controlled by agents.”

Source: CoreLogic

Mike prompts the underquoting debate also… perhaps this is a good topic for another episode! Stay tuned.

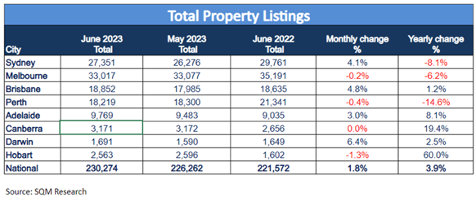

Hobart and Canberra are the two capital cities that have bucked the trend and had strong listing activity. This supply and demand imbalance is reflected in the growth data, unsurprisingly.

Mike asks Cate and Dave about distressed listings, and despite the media suggestions that the fixed rate cliff and the increased interest rates could give rise to distressed listings, Cate points out that this is not occurring, and the data supports this.

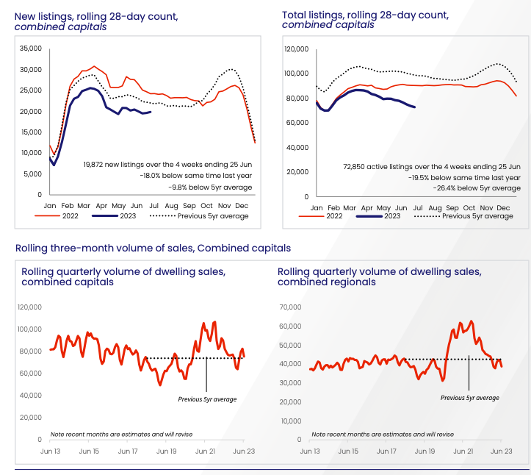

And the CoreLogic findings for new listings vs total listings is telling. New listings are still well below the historical five year average, however the total listing figures have nose-dived. This illustrates an increased buyer appetite for old listings, (those with greater days on market than 180 days), a sure sign that buyers are outstripping sellers.

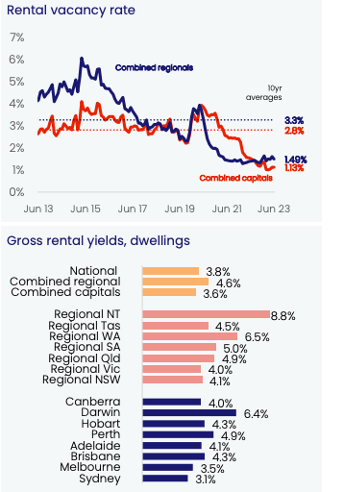

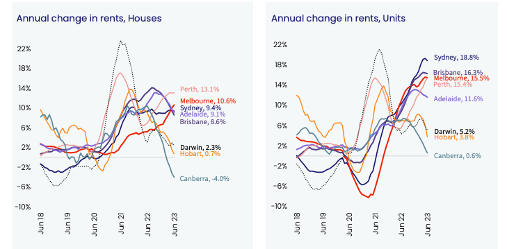

Mike asks Cate to comment on the vacancy rate data. A slight amount of easing is evident in some markets, but as Cate points out, “there are markets within markets” so the data is not entirely reliable. Melbourne is still surging with house rents, and units remain tough propositions for renters. Dave suggests that migration (both internal and overseas) are still contributing to the rental issue.

Mike does challenge the relationship between new arrivals and unit rents; it’s an interesting conundrum.

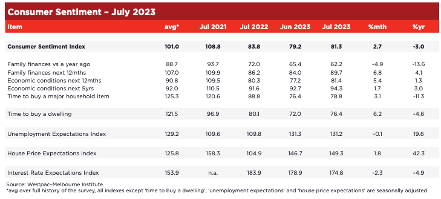

The Westpac Consumer Sentiment data is out, and it’s somewhat puzzling for the Trio.

Dave adds perspective to the house price index figure by explaining how optimistic the general public actually are.

Cate’s ‘toys’ index is a concerning figure. We are still spending, and the increasing interest rates haven’t curtailed our attitudes towards spending like our RBA wish they would.

As Mike says, “It’s the buying-stuff activity that is keeping our inflation high.”

Lastly, Dave shares some clever data about purchase activity. It might surprise our listeners! Tune in to hear more.

And… time for our gold nuggets…

Dave Johnston’s gold nugget: Dave summarises the market by saying price growth is slowing down, but it’s still positive. He also touches on investor-led sales and he hints at supply of new listings increasing… happy news for the buyers out there. However, upgrading remains a challenge for a large cohort of buyers.

Cate Bakos’s gold nugget: We have a segmented market and the renovation projects remain a significant challenge while builders and trade materials are in limited supply.

Mike Mortlock’s gold nugget: it’s an uptick in sentiment, and an uptick in investors getting out of the market.

Resources:

If you’ve enjoyed this show, take a listen to these eps:

10 – Why your approach and assessment of risk is paramount to property success!

19 – TIME IN the market v TIMING the market

31 – Get rich quick schemes: #1 of the top seven critical mistakes