Ep. 279: Market Update Sep 24 – National Price Growth Slows, Rents Drop to 4-Year Low, Is Perth Finally Slowing as Listings Boom Nationwide?

Ep. 279: Market Update Sep 24 – National Price Growth Slows, Rents Drop to 4-Year Low, Is Perth Finally Slowing as Listings Boom Nationwide?

Mike kicks off this episode, and after stumbling with Cate’s surname (yes, he’s on fire with names), the Trio crack into the market update for September.

“Is this the beginning of the peak or decline for these markets?”

Perth’s rate of growth has slowed, and the Trio ponder whether it’s listing numbers, tightening household savings, or interest rate pain that is contributing.

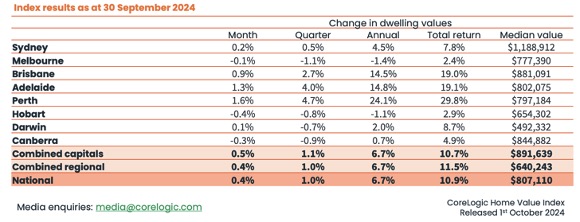

How long can the three top performers maintain this strength? And are they at their peak? Perth’s annualised growth is currently sitting at 24.4%, which is significant by any historical measures.

Taking the Reserve Board’s monthly press releases into account is important. Until we return our inflation numbers to a figure within the target band, our interest rate pain is likely to remain.

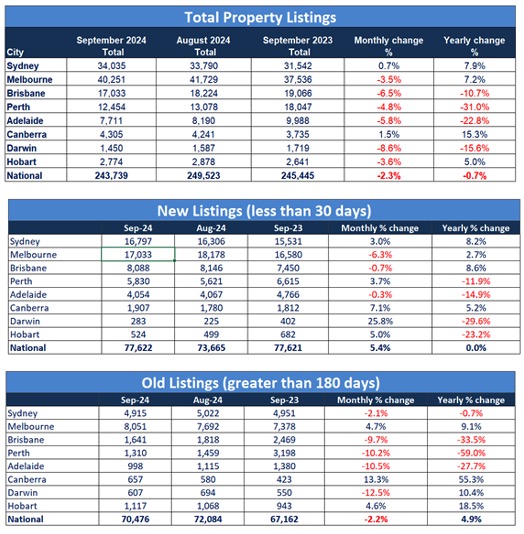

Dave sheds light on net overseas migration numbers and draws a parallel with the slowdown in price growth, and the Trio overlay the listing figures that are amplifying the supply/demand imbalance.

Mike and Cate chat about mean reversion and some of the weaknesses of this popular argument. Just because Darwin hasn’t performed well over many years, does not mean that Darwin’s ‘turn’ is next. There is more to mean reversion than just labelling a slow performer ‘the next one’.

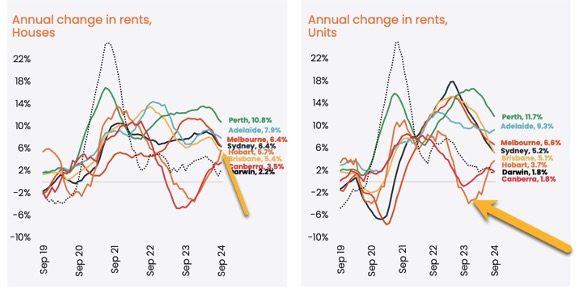

Rental pressure continues to soften. What could explain Hobart’s pattern? Rents have all come off the boil with the exception of Hobart. Cate has some insider insights….

Will pressure on rents continue to ease? As Dave mentions, household formation rates are playing a powerful role in the rental numbers also. Cate ponders the impact of student numbers and the effect on market segments, specifically inner-city apartments.

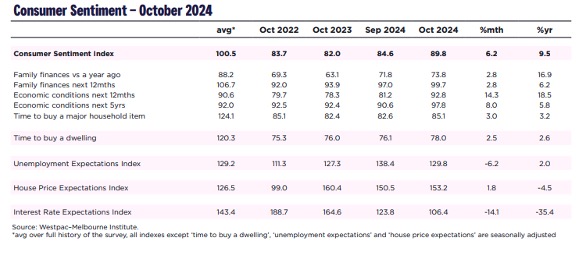

The key takeaways from the consumer sentiment index include ‘Time to buy a dwelling’. The WA figures are interesting in particular. The ‘Interest rate expectations index’ has dropped substantially, and once again, the differences across the states and territories might be telling us a valuable story.

Sentiment counts for a lot, and Cate considers the impact of the anticipation for a rate cut during September. The House price expectation index was another that the Trio noted and Dave noted WA’s and QLD’s softening for this measure, and contrasted it against Vic’s and NSW’s uptick.

And we’ve hit the highest number of new investor lending commitments that we’ve seen since Jan 2022 this month, and as Dave points out, “That was back when the cash rate was just 0.1%.”

Are first homebuyers getting enough support?

Shared equity… yeah/nah? The Trio chat about some of the government led initiatives that offer some support to first homebuyers.

And… time for our gold nuggets…

Cate Bakos’s gold nugget: The rate of change of rental growth is easing and it will be interesting to see how this filters through into political policies.

David Johnston’s gold nugget: “Markets are cyclical. No market is always flying or always struggling. Have a long term plan when you’re buying property.”

Mike Mortlock’s gold nugget: When it comes to first homebuyer activity, it seems that we’re addicted to stimulatory stuff. But we don’t tend to have many policies that help with supply.

“We need to attack the supply issue, rather than stimulus, stimulus, stimulus.”

Resources:

If you’ve enjoyed this show, take a listen to these eps:

6 – What determines your Property Strategy

10 – Why your approach and assessment of risk is paramount to property success!

18 – When to hold and when to fold!

60 – Why established properties outperform

Charts sourced from Core Logic, ABS and SQM