Ep. 288: Market Update Nov 24 – Perth, Brisbane & Adelaide Slow, Listings Surge in Adelaide and Perth, Rate Cut Predictions & Productivity Woes Persist

Ep. 288: Market Update Nov 24 – Perth, Brisbane & Adelaide Slow, Listings Surge in Adelaide and Perth, Rate Cut Predictions & Productivity Woes Persist

The Trio are back together in the studio!

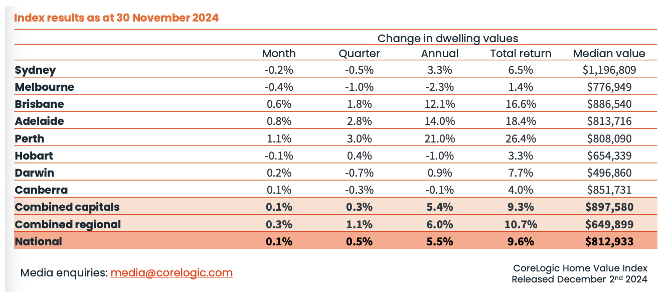

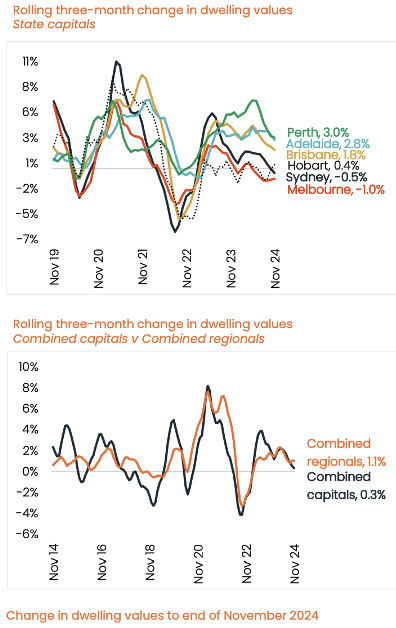

The Trio comment on some of the interesting indices for the state of the nation in the month of November. Cate marvels at regional performance outstripping capital city performance. The big tier, top three cities are showing weaker growth and Melbourne has continued to show modest price falls.

Dave predicts that 2025 could be the story of Melbourne and Hobart. He shares his rationale… let’s see how his prediction lands!

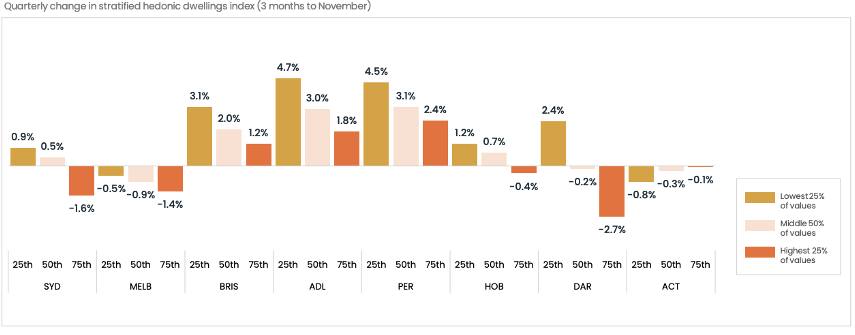

Mike points to the stratified price figures and notes that the lowest quartiles are outperforming, all but for ACT and Dave touches on the per capita recession we are all currently in. Canberra’s public servant population defies this trend.

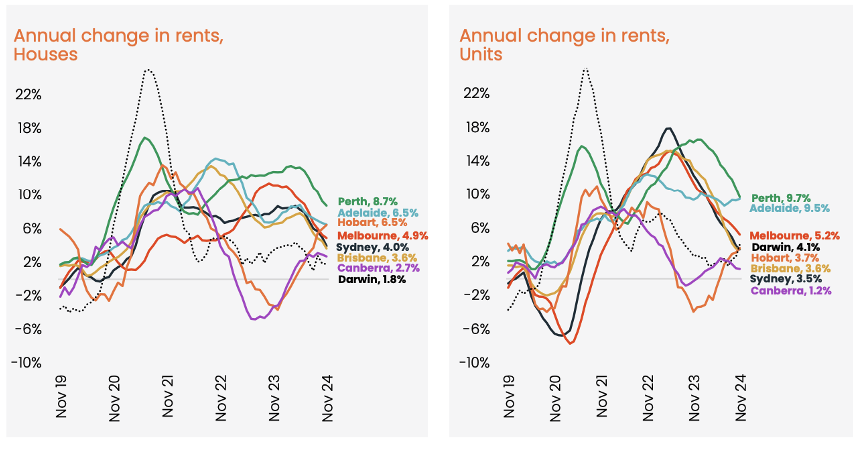

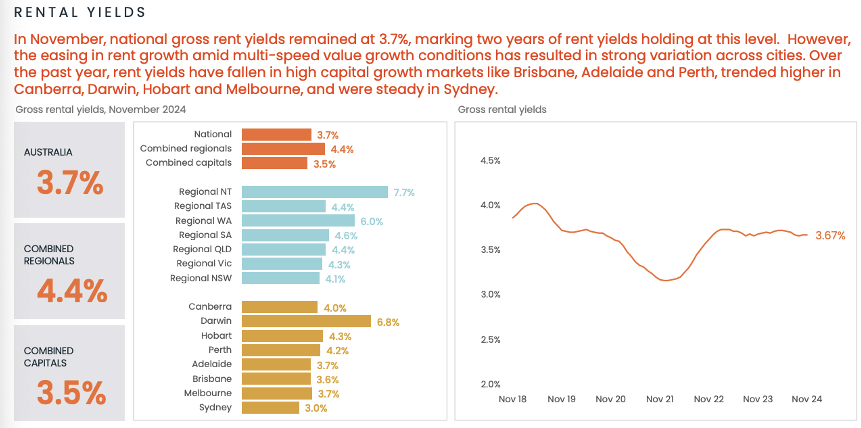

Rents are dipping, but they are all still in positive territory, as as Cate mentions, the rental growth is still outstripping CPI.

“Any other precedent would say that these are huge numbers, but they’ve come off the boil a long way,” says Mike.

Rental increases now are normalised now though, and as Peter Koulizos has said before, rents had to play catch-up.

Rental yields have decreased substantially for many regional cities, and Cate considers some of the challenges and changes that have impacted quite a few regional markets since COVID lockdowns.

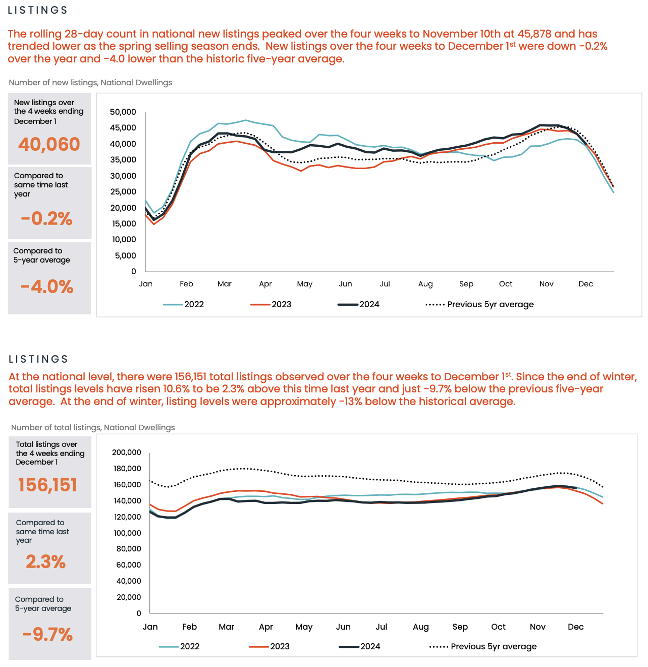

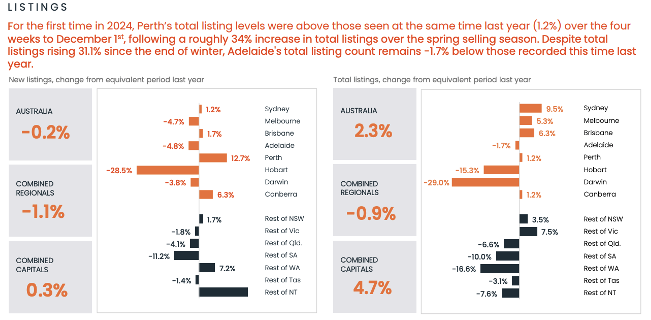

Sales and listing activity is a great insight into market supply. Cate doesn’t expect listing figures to dramatically increase and she hints that pent up demand could show itself in early January in the larger markets. Could the start of 2025 be a bit different to recent past years? Tune in to find out.

Contrasting the listing figures from October to November tells an interesting story too. Hobart’s decrease in listings when contrasted against this time last year is significant. What is happening in Hobart?

The Trio chat about the pressure on the RBA to control monetary policy, and they consider the key drivers and data points that our RBA are keeping a close watch on. From productivity to services inflation, unemployment to public sector job growth, (just to name a few) there are plenty of moving parts that remain a challenge.

The quarterly GDP figures are out for the month of September and the strongest segment leading the charge is Agriculture, Forestry and Fishing at 6.5%.

Lastly, the Trio share their thoughts on when the next rate movement could be!

Resources:

- Related eps:

- 6 – What determines your Property Strategy

- 10 – Why your approach and assessment of risk is paramount to property success!

- 12 – Property Cycle Management – why now is always the best time to buy if it suits your personal economy and you have a long-term property plan

- 18 – When to hold and when to fold!

- 60 – Why established properties outperform

- Upcoming ep – 289 Listener Question on Shared Equity Scheme

Charts sourced from Core Logic, ABS and SQM