Ep. 218 – Market Update July 23 – Rental growth slows, will rent freezes fan the flames, exploring the office exodus & capitals thrive as regionals dive

Ep. 218 – Market Update July 23 – Rental growth slows, will rent freezes fan the flames, exploring the office exodus & capitals thrive as regionals dive

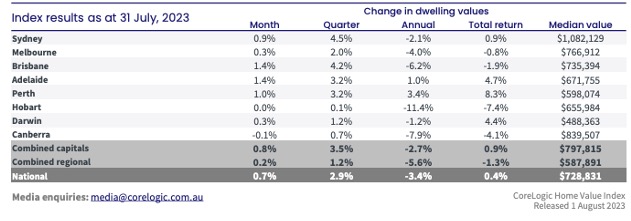

Cate points out that the capital cities have outperformed the regional cities of late, and Dave draws our listener’s attention to the sheer performance of Brisbane, Adelaide, Perth and Sydney when contrasting the median value ladder places. Despite the upturn, many major cities are still beneath their cyclical highs.

Cate’s discussions at the coal face signal that some of her listing agent friends are quite busy with their appraisal activity – always a precursor to higher listing volumes. Mike quizzes Cate on this leading indicator and it’s something all buyers can take a pulse on when chatting to agents, but data is also available on CMA report generation; a great relationship to note between appraising and listing.

And Mike circles Perth as a discussion point. Dave and Cate are reluctant to suggest that Perth’s outperformance will sustain longer term, but both agree that the combination of growth and yield hold Perth in a ‘watch this space’ category.

Mike quizzes Cate on the movement from the regions back to the city and Cate corrects Mike’s assumption. The viability of country-life hasn’t necessarily changed for those who moved away from the city during lockdowns, but now that bosses are calling their staff back to the office, many buyers are buying a ‘second home’ option as their city pad. Cate shares a recent client’s purchase; a $365,000 unit in Melbourne’s Footscray. With an appraised rental of $380pw, an asset like this demonstrates that 5%+ returns are possible in Melbourne.

Cate’s concerns about depleting rental stock are attributed to a few factors, including higher divorce rates and city-pad, part-time dwellers.

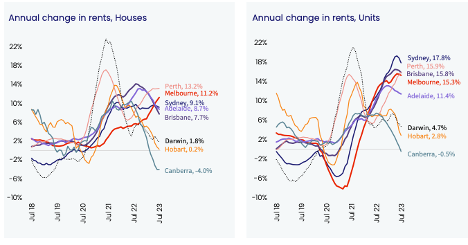

Dave speaks about the rate of rental increases easing, but still cautions the state governments to consider the negative consequences of rent freezes. Cate discusses the need to consider each market separately, given that different drivers and threats are destabilising some markets more than others.

“If you are a tenant and you’re copping a 15% rental increase each year, you’ll absolutely feel it”, says Cate.

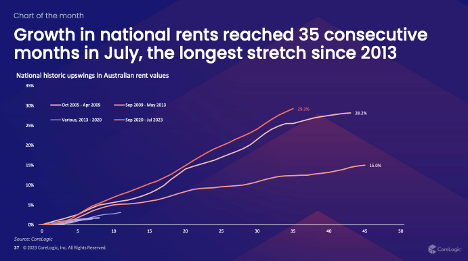

The trio discuss the fact that growth in national rents reached 35 consecutive months in July – the longest stretch since 2013.

Source: Core Logic

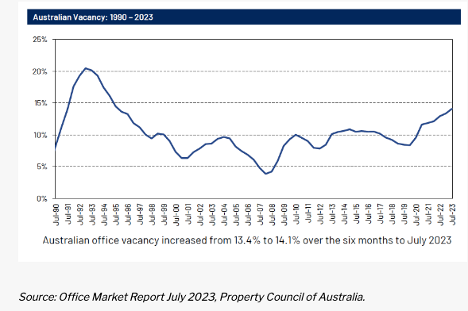

The Trio chat about ‘optimal’ vacancy rates and all agree that 2-3% signifies a healthy rental market.

Cate threw in an Office Vacancy chart to share with Mike and Dave. The chart shows some significant vacancy rates (circa 13%) and Cate explains why office vacancies are so contrasted from residential vacancies. Tune in to hear why….

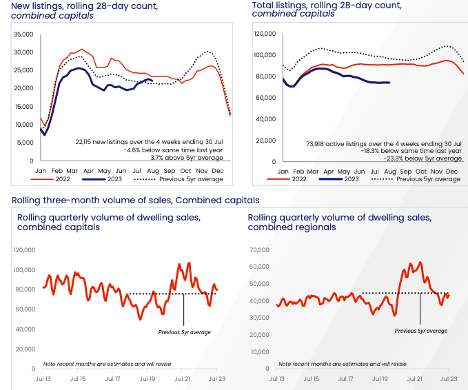

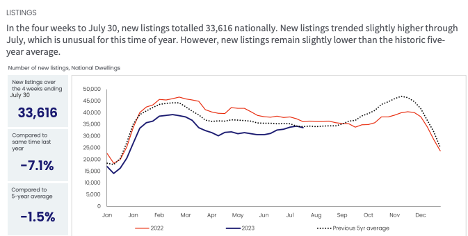

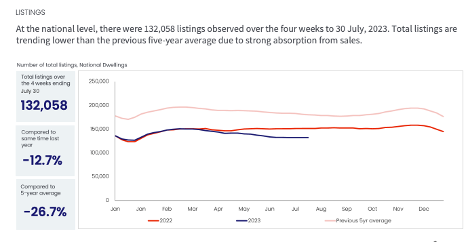

Dave and Cate discuss the Spring market and ponder whether buying conditions will improve during this season. Cate circles October/November as her ideal buying months for 2023, and notes that listing numbers have improved through the months of July and August.

As the “All listings” chart shows, however, buyers are still soaking up the listings and buyer demand still outstrips seller motivation.

The Westpac Consumer Sentiment data is out, and it’s somewhat puzzling for the Trio.

“Time to buy a dwelling” is slightly higher, while sentiment shows that house price expectations show that we expect house prices to go up.

“I wish I could, but I can’t” suggests Mike as a good explanation for this unusual set of data.

Cate’s ‘toys’ index has still slightly gained. Trips to Europe seem to be the flavour of the day for a lot of people.

Lastly, Cate shares some extra observations for our listeners; an uptick in first home buyer activity, low dwelling approvals, reducing distressed listings, and a troubling increase in personal (unsecured lending). These all tell an interesting story in their own right. Tune in to hear more.

And… time for our gold nuggets…

Dave Johnston’s gold nugget: Dave talks about some of our two-speed markets, citing the Gold Coast, South-East Tasmania and Newcastle/Lake Macquarie as high performers, and he delves into some slow performers in Victoria. There really are markets within markets!

Cate Bakos’s gold nugget: Cate anticipates higher listing figures in Spring and feels that the 2023 opportunity for buyers could match late 2022’s.

Resources:

If you’ve enjoyed this show, take a listen to these eps:

Ep. 10 – Why your approach and assessment of risk is paramount to property success

Ep 52 – Dissecting ten years of CoreLogic data

Ep. 61 – Commercial property part 1 – the risks and the rewards

Ep. 205 – April 2023 Market update – budget night and rising rents… how do we solve the issue?